Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

November, 2022

Why Are Mortgage Rates Still Rising And How Much Higher Will They Go?

(Charts courtesy of Keeping Current Matters)

Mortgage rates are one of three key drivers of today’s real estate market. The other two being supply vs. demand and home values. And both buyers and sellers are wondering if mortgage rates will continue to climb higher and if it is the time to jump into the market, either to buy or sell. Here is where mortgage rates are as the beginning of November, and where experts believe they will be heading in the months ahead.

Why Rates Are Still Climbing In November?

Higher mortgage rates are a response to high inflation. Inflation escalated in early 2022, with gasoline prices spiking, housing and rent prices jumping to unprecedented levels, and food and other consumer goods sharply increasing. The effect was consumers suffered, bought less, and paid more for their daily needs.

Economists suggest that the Federal Reserve recognized higher inflation in 2021. However, they thought this inflationary environment was temporary due primarily to supply chain issues caused by the pandemic. While this was an important factor, it was not the only one.

Government spending and the Russia-Ukraine conflict also played a role. In addition, China continues to lock down commercial and residential areas due to its zero-Covid policy and inflation shot up. In response, the Fed started a series of interest rate hikes to combat inflation and ultimately reduce the amount of money circulating in the economy.

Although raising interest rates does cause financial pain for consumers and businesses, inflation would have been worse if the Fed had not started to raise rates. It would have made a bad situation even harder for people to buy necessary and discretionary goods and services. With that said, the Federal Reserve is running the risk of creating a recessionary environment by keeping interest rates too high. It can increase unemployment, and as seen, run havoc with the real estate market as mortgage rates keep pace with the Fed fund rate.

The Latest Rate Increase, November Meeting

On November 2, 2022, the Federal Reserve raised their Fed fund rate by another 75 basis points or three-quarters of one percent. That brought the current rate to a range of 3.75 percent and 4 percent. Economists and others were expecting this level of increase, so mortgage rates did not adjust by an equal amount. During the Fed’s Chairman briefing, Jerome Powell did hint at the potential of slowing down the rate of future increases. As such, smaller hikes may be forthcoming, but a complete pausing of hikes is probably not in the cards.

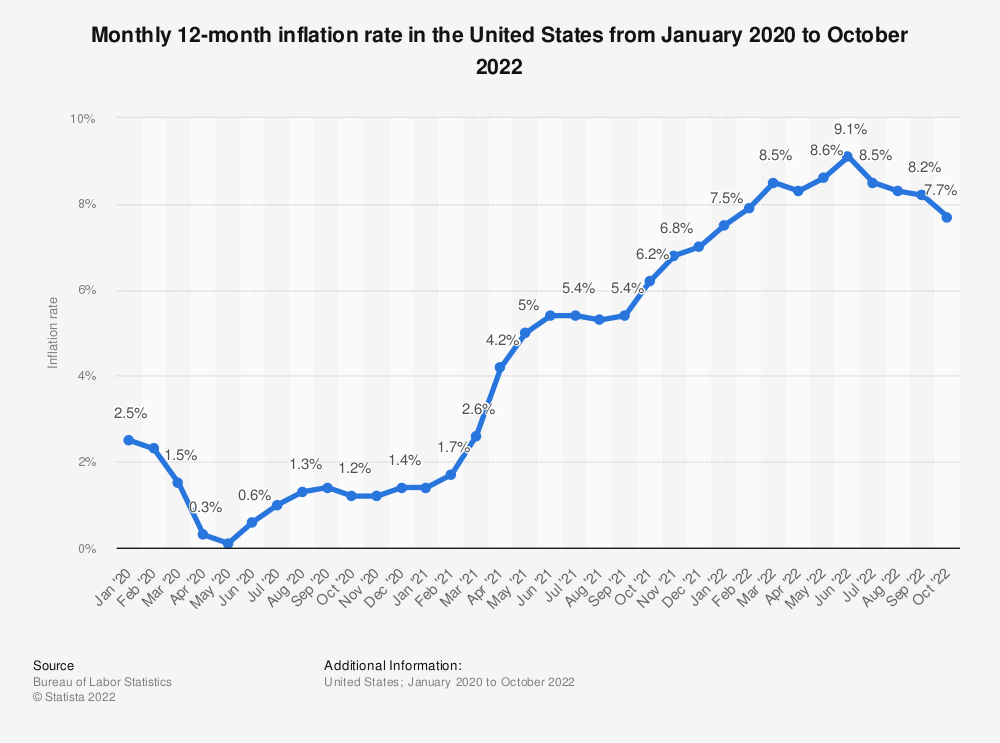

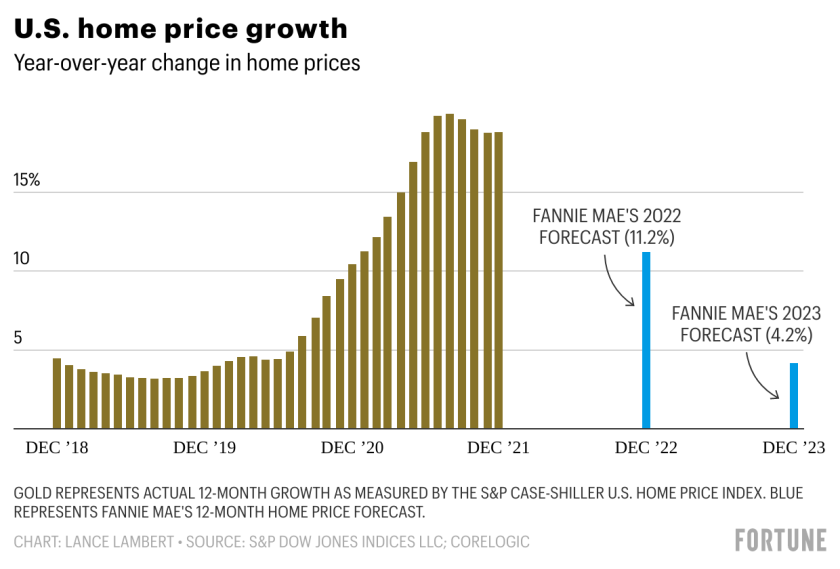

The only way the Fed will probably stop hiking, or begin lowering its Fed fund rate is if the economy shows definitive signs that inflation is returning to a more acceptable rate. And that is in an annual range of 2 to 3 percent. As of October 2022, inflation had move

d to 7.7 percent compared to a year earlier. That is down from 9.1 percent reached during the this past summer (see chart on right).

How Much Higher Will Mortgage Rates Go?

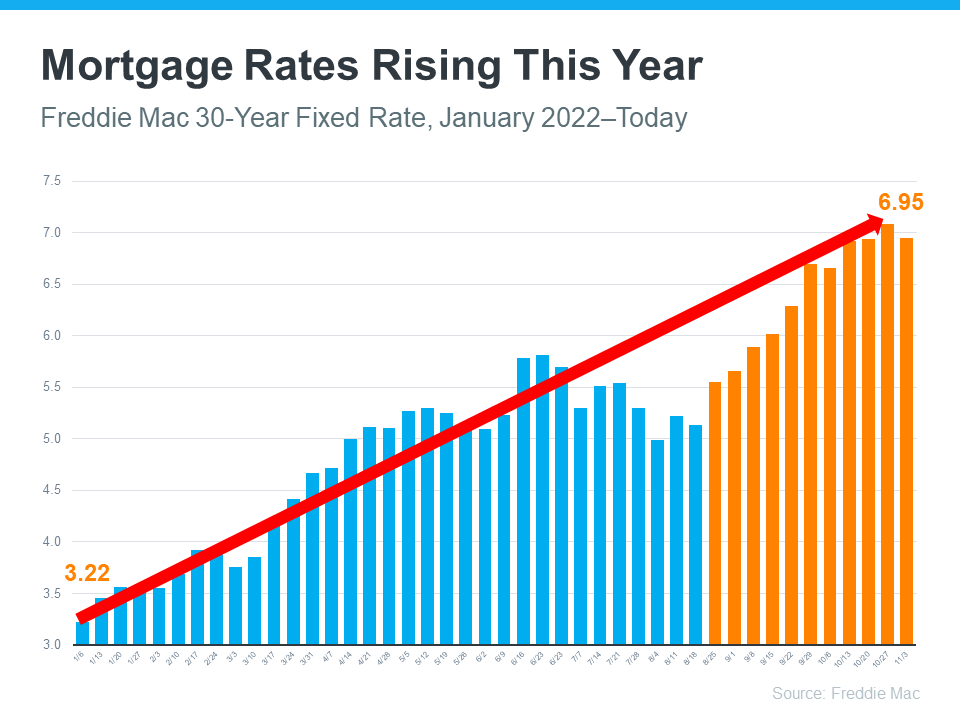

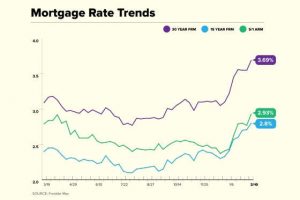

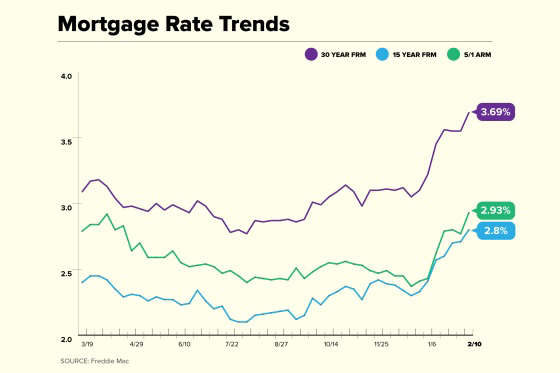

The chart on the right shows the Freddie Mac 30-year fixed rate from January 2022 to the beginning of November. The chart shows what the real estate market has felt. Rates have been climbing dramatically this year. Although rates have ticked back slightly from its high of over 7 percent, economist believe that rates will remain in the 7 percent range for the reminder of 2022. However, what happens after this year is dependent on what the Federal Reserve does. If they slow down the pace on increases, 7 percent could be the rate well into 2023. However if they sense inflation is under control and lower rates, mortgages could fall below 7 percent. Likewise, if inflation remains stubborn and the Fed raises by another 75 basis points, or more, rates will experience upward pressure through the end of next year.

This runup in mortgage rates has slowed the overall real estate market. Some areas more than others. So far, Bridgewater and the surrounding areas have seen some slowdown but buyer demand is still there. And supply continues to be tight (see below) so there are less homes for buyers to choose from which keeps demand for those homes strong. But the rise in rates has caused some buyers to pause their plans and others to be more deliberate in their purchase.

If there is a positive spin to the rise in rates, it comes from Mark Fleming from First American, a financial company providing title insurance and professional settlement services to home buyers and sellers, when he said “While mortgage rates are expected to continue to drift higher over the coming months, much of the rapid increase in rates is likely behind us”. Although rates may feel upward pressure, buyers and sellers should not worry about rates doubling again like they have seen this year. Mortgage rates will respond to Fed decisions on inflation, but it should not be expected that the market will see exponential increases like before.

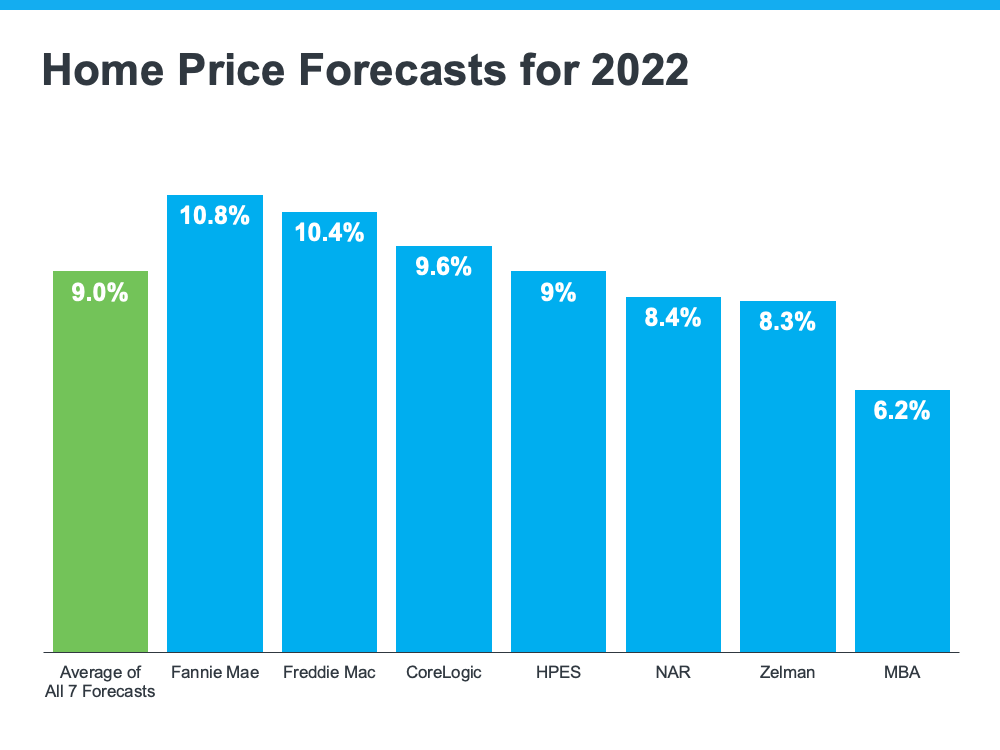

So What About Home Prices?

So what does the above mean for home prices. Refin, a large residential real estate brokerage, was quoted as saying, “For those bearish folks eagerly awaiting the home price crash, you’ll have to keep waiting. As much as demand is pulling back, supply is as well. And that’s reducing downward pressure on prices in the short run”. This means that the balance between supply, the amount of homes on the market, and demand, the amount of buyers, is the king for what happens to prices. And this is a variable that is not the same in all areas. It is highly local. What is happening in Phoenix or Las Vegas, may not be the same as in Bridgewater.

In some areas, showings are down and home price appreciation has decreased (not the same as depreciation). In others, demand is still high with multiple offers still the rule.

Currently in Bridgewater, the demand for homes, while diminished due to mortgage rates and affordability issues, is still high. The majority of homes are off the market in under 25 days and supply is still tight, only 1.71 months in October, slightly up from 1.49 in September. In addition, 66 percent of homes sold last month were above listed price. With this kind of market, there is little reason to believe homes will not continue to see price appreciation in the coming months, albeit tempered from increases in the teens during the past couple of years.

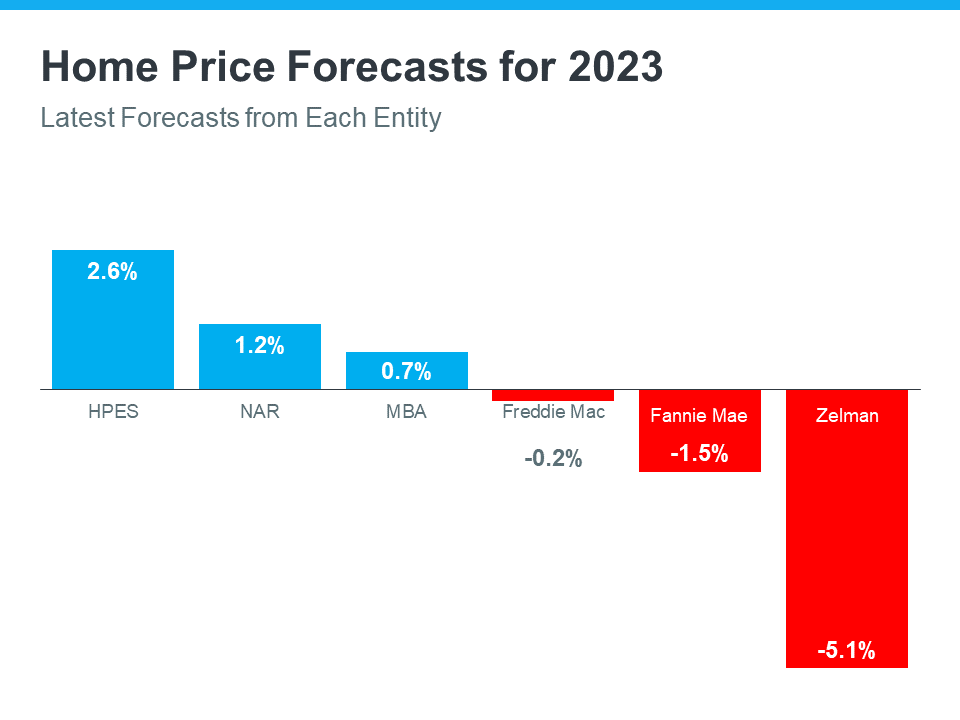

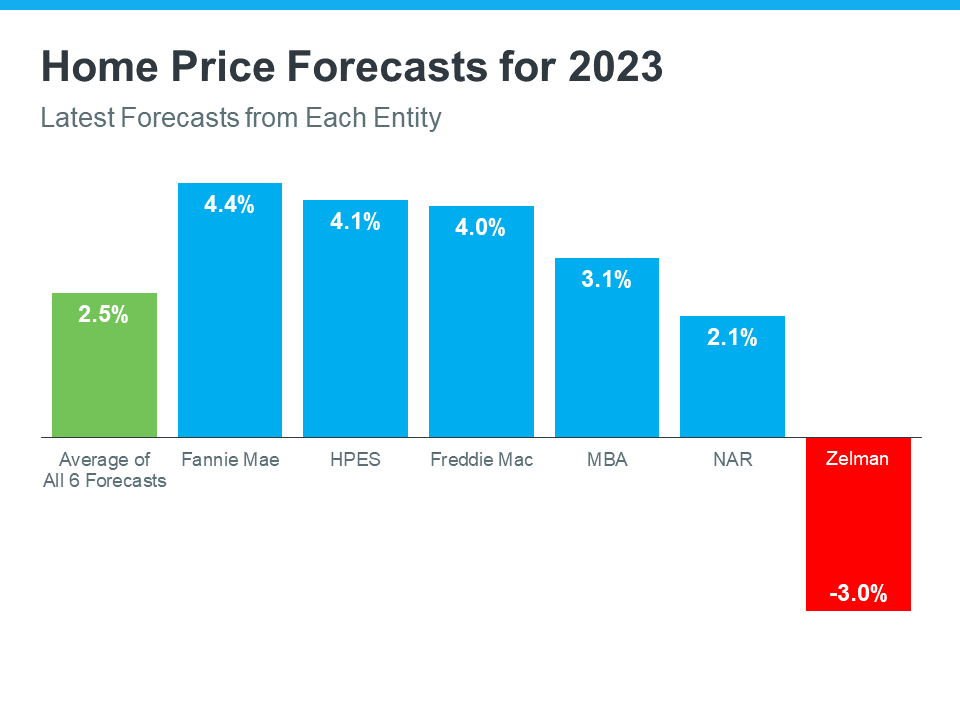

Nationally, experts have cooled slightly on the 2023 market from last month. Forecasts range from a price increase of 2.6 percent to a negative 5.1 percent. So, when averaged, they are looking at a more neutral market. But these numbers should be balanced against local conditions.

{kind=link}