Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

February, 2022

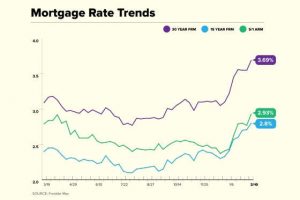

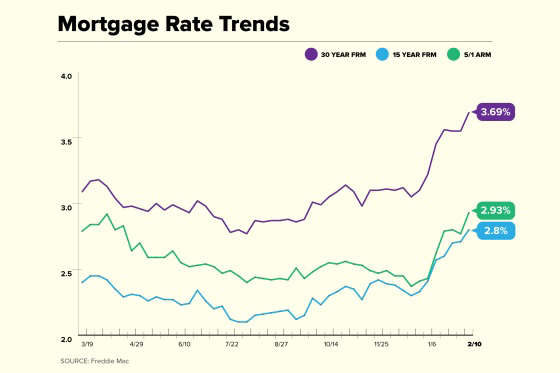

Mortgage Rates Are The Story

Readers of Market Watch were aware that mortgage rates would increase over the course of 2022. In last month’s Market Watch it was noted that “Many economists expect mortgage rates to rise this year after the Federal Reserve announced last month that it would begin dialing back its monthly bond purchases, which was intended to lower long term rates to help slow accelerating inflation. In addition, experts expect continuing economic growth and the tight labor market to continue to push rates higher.” The conclusion was that rates to reach 3.5 percent by the third quarter and up to 3.7 percent by the end of the year.

Well, mortgage rates did rise this past week, but well above forecasts. In fact, rates just had the largest one month jump since 2013. According to Freddie Mac, whose mission is to promote stability and affordability in the housing market by purchasing mortgages from banks and other loan makers, rates for a 30 year fixed mortgage had jumped from 3.11 percent at the end of December to 3.55 percent on February 3, and to 3.69 percent, with 0.8 points paid, one week later. The average rate was 2.73 percent at this time last year.

The rate for a 15 year mortgage also saw a significant increase. Rates increased by 0.16 percentage points during the February period, hitting 2.71 percent, with 0,8 points paid, on February 10. The average rate was 2.19 percent during the same time period last year.

The situation is more hard hitting if points are taken out of the equation. In that case, rates are being quoted as high as 4.02 percent.

The upward pressure is likely to continue. The consumer price index, released on the February 10, showed that inflation increased to 7.5 percent compared to the 7.2 percent estimate from market observers. That is the highest rate of inflation since 1982. As a result, Treasury yields are rising, and if that continues mortgage rates will follow.

Will the rise in rates shake up the home buying market? Because of the high demand for homes, and the very low inventory, the market should not significantly suffer. Affordability will become an issue for some buyers. And some may drop out. Take a $500,000 home purchase with $100,000 down, a 30 year fixed rate mortgage at 3.0 percent is $1,686 (not including taxes etc.). At 3.69 percent, the payment jumps to $1,839, a $153 monthly difference.

Not only could that higher monthly payment scare off some would be buyers, it will also lock some buyers out of the market. That is because banks and other lenders issue mortgages based on strict debt-to-income ratios, which include the mortgage being applied for. That means that each time mortgage rates increase, even by a small amount, some buyers lose their mortgage eligibility.

{kind=link}