Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

October, 2022

Economic Uncertainty And The Housing Market

(Charts courtesy of Keeping Current Matters)

Will there be a recession? Will the Federal Reserve raise their rate again? If they do, by how much? Will mortgage rates increase? If so, by how much? What will happen to housing prices? Will my home lose value in the coming months? Should I sell/buy now or wait?

These are the types of questions asked when talking with those looking to buy a home in a market with rising

mortgage rates and challenging real estate prices, and existing homeowners questioning whether to take advantage of past appreciation and sell, or hold on until rates decrease stimulating more demand.

And they are great questions, all pointing to the uncertain economic climate and what affect it is having on the

housing market. This Market Watch will not attempt to answer all the issues surrounding today’s real estate market,

but it will provide insight into three areas of home buyer/seller concern.

1. Will there be a recession and what affect will it have on the housing market?

2. Where will interest rates go from here?

3. Will home prices increase or decrease in the months ahead?

Will there be a recession and what affect will it have on the housing market?

There is concern within the business and consumer sectors that a recession is on the horizon. The Federal Reserve has already increased their Fed Fund Rate to 3.25 percent, with the last .75 percent increase authorized during their September meeting. The concern is if the Federal Reserves raises further, it could push the economy into a recession.

In their attempt to bring inflation to their targeted 2 percent area, all indications are that the Federal Reserve will raise their rate by .5 to .75 percent at their next meeting, which is November 2. In all probability, that will slow the economy further, and increase the chance of drawing the economy into a recessionary period, or at least on the brink.

A movement in the rate will increase borrowing costs for both businesses and consumers from commercial loans, to credit cards, and yes probably mortgage rates. A rate increase will further slow home purchases and price appreciation (not depreciation) due to its impact on overall affordability. That would be bad for the economy because of the tremendous impact the real estate market has on the economy, not just in home sales, but also subsequent purchases such as furniture, décor etc.

Once the Federal Reserve achieves its goal of reducing inflation, it will need to pull the economy out of the recession. To do so it will reduce its fund rate and mortgage rates will fall. In fact, over the past six recessions, mortgage rates have fallen an average of 1.8 percentage points, with some dropping considerably more, from the peak of the recession to the trough. And in many cases they continued to fall after the fact, since it takes some time to turn the the economy around. It is often said that housing will lead the economy out of recession. And historically it has. The economy will not recover until housing leads the way out. Housing has that much impact on the economy. And the Federal Reserve recognizes that.

The graph below indicates the dates of the six recessions, their length, and how much mortgage rates fell. In each of the past recessions,

mortgage rates dropped, stimulating the economy. Hopefully, history this time will repeat itself.

Where will interest rates go from here?

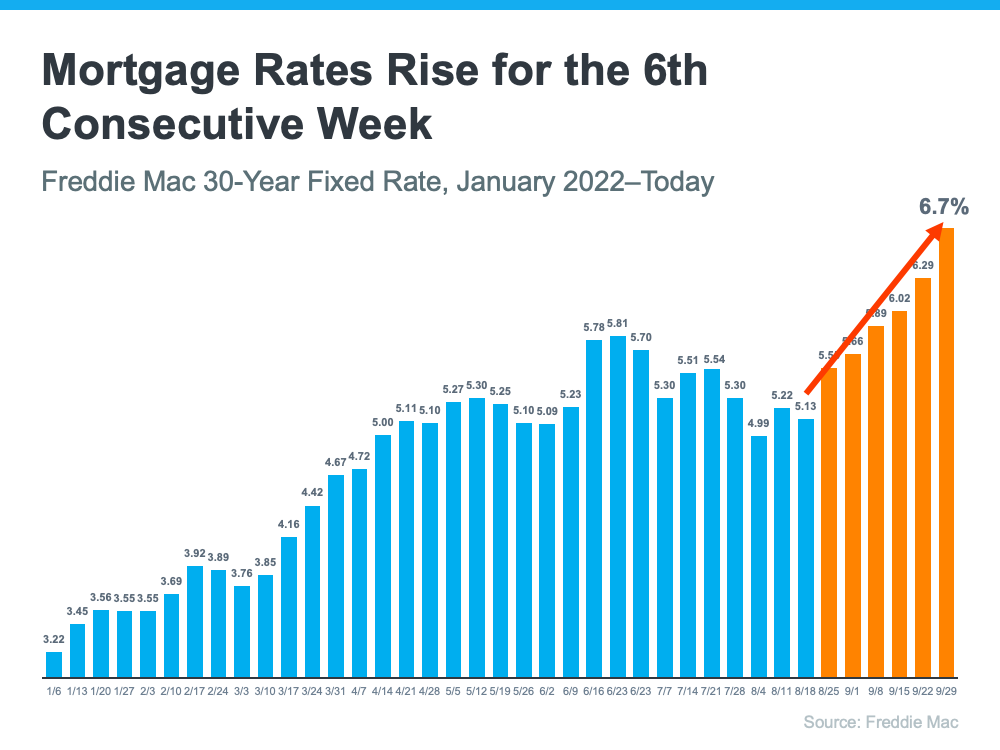

A large part of the fear and uncertainty people have right now in the housing market is the question of where mortgage rates are going. Or, better put, will mortgage rates continue to rise? And a large part of this uncertainty is what they are seeing in the media. Almost daily they are seeing headlines such as the housing market in for another shock. Mortgage rates reach highest level since 2008. 30 year mortgage rate jumps over 7 percent. Headlines like these create fear and uncertainty and cause potential sellers and buyers to pause any plans.

So the question is, where are rates heading? The news here is not the best. The graph below is the Freddie Mac 30 year fixed rate from January of this year, all the way through the end of September. It shows that rates rose for sixth consecutive weeks (orange bars), reaching 6.7 percent. Since then, mortgage rates have continued their upward climb with 30 year rates reaching 7 percent with some

lending institutions quoting higher rates.

The reason rates have been rising is due to the Federal Reserve raising its Fed Fund rate to tame inflation. They are trying to slow the economy, and their weapon is the Fed Fund rate. Even though the Fed does not set mortgage rates, their action in raising its rate is having an impact on mortgage rates. And it is working as the real estate market has slowed.

Where do rates go from here? Mortgage rates tend to rise with the rate of inflation. When inflation is high, so are mortgage rates. Inflation is the enemy of long term interest rates, and that is exactly what is happening today. So until inflation is down significantly, mortgage rates will stay stubbornly high, and will probably hover just over 7 percent. But as for good news, Mark Fleming, Chief Economist at First American, a provider of property and mortgagerelated services, states “While mortgage rates are expected to continue to drift higher over the coming months, much of the rapid increase in rates is likely behind us”.

Will home prices increase or decrease in the months ahead?

David Ramsey, a personal finance expert and host of The Ramsey Show, said it best, “The root issue of what drives house prices almost always is supply and demand”. And this is a variable that is not the same in all areas. It is highly local. What is happening in Dallas, may not be the same as in Bridgewater.

In some areas, showings are down and home price appreciation has decreased (not the same as depreciation). In others, demand is still high with multiple offers still the rule.

Currently in Bridgewater, the demand for homes, while diminished due to mortgage rates, is still high. Homes are off the market in under 25 days and supply is only 1.49 months. In addition, 63 percent of homes sold last month were above listed price. With this kind of market, there is little reason to believe homes will not continue to see price appreciation in the coming months.

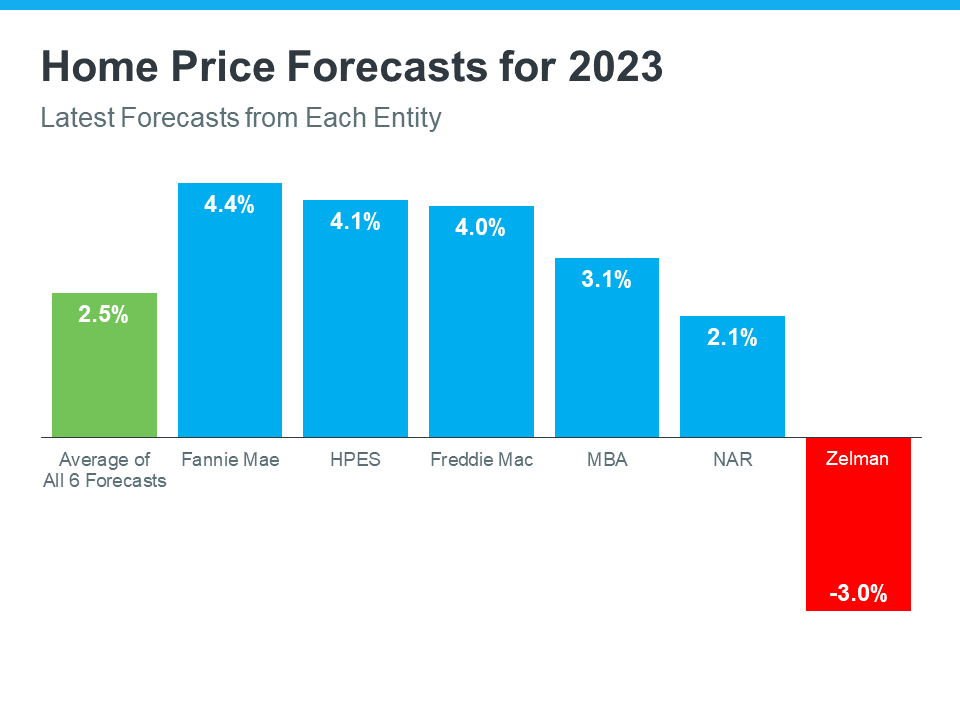

Experts predict that 2023 will see price increases ranging from 4.4 percent to a negative 4 percent, But 5 out of 6 expect price increases with the average of the 6 forecasts being 1.8 percent. So expectations are that homes will continue to gain value, just at a slower rate from the last couple of years.

{kind=link}